BB Desk

Country’s total office stock is expected to cross the historic one billion square feet (bn sq ft) in office supply by Q3 2025, states the Knight Frank exclusive report- A Billion sq ft and Counting– India Office Supply Growth Story. This will mark a significant milestone in the office real estate market and move India’s stock closer to that of other international gateway markets. From under 200 mn sq ft in 2005 to nearly 1 bn sq ft in 2025, office supply has grown at a CAGR of 8.6% in the last 20 years. The expansion underscores India’s emergence as one of the fastest-growing and most future-ready office market globally.

The report highlights how India’s office market has scaled both in volume and quality. It attributes this success to long-term economic fundamentals, favourable demographics, digital transformation, and a sustained focus on developing high-quality, sustainable workspaces. According to the report, the cumulative office stock across the top 8 Indian cities stood at 993 million sq ft. Bengaluru leads with 229 mn sq ft (23%), followed by NCR with 199 mn sq ft (20%) and Mumbai at 169 mn sq ft (17%). Bengaluru, NCR, and MMR have led this expansion, collectively accounting for 60% of the total stock. Close behind, Hyderabad, Pune, and Chennai contribute another 33%, while Ahmedabad and Kolkata make up the remaining 7% of India’s office stock.

Evolution of India’s Office Market

India’s office demand has transformed dramatically from 1990 to 2025, evolving from a tech-industry support base into a global hub for capability centres, rising in the value chain. Spanning seven distinct phases, this journey reflects resilience, innovation, and policy-led reform. Milestones like the SEZ policy, regulatory improvements, and infrastructure investments have enabled the market to reach the 1 billion sq ft mark—underlining scale, quality, and institutional depth. However, to bridge India’s office growth gap, policy and capital interventions are needed to address supply constraints, or risk rental inflation, occupier shifts, and missed investment opportunities amid rising demand.

“As we prepare to cross the 1 billion sq ft threshold, it’s not just a number, it reflects the growing institutionalisation, maturity, and global relevance of India’s office market. This transformation has been powered by an ecosystem of world-class developers, investors, and occupiers who have continually raised the bar in creating dynamic, sustainable workspaces. It also reinforces India’s positioning as a global economic powerhouse, offering a compelling value proposition for multinational businesses and institutional capital.” saysShishir Baijal, Chairman and Managing Director, Knight Frank India.

India’s Sub-Dollar Advantage

A defining competitive edge of India’s office market lies in its remarkable cost efficiency, especially when benchmarked in dollar terms. India’s office market offers a unique cost advantage, with average rents declining to USD 0.96/sq ft/month in 2025, reinforcing its sub-dollar status globally. This affordability, paired with rising Grade A supply, has accelerated the growth of GCCs. As global occupiers seek cost-effective, high-quality, ESG-compliant workspaces, India’s value proposition continues to strengthen its strategic role in corporate real estate portfolios.

India’s Office Stock: National Overview

Commenting on the occasion, Gulam Zia, Senior Executive Director- Research, Advisory, Infrastructure and Valuation, said, “India’s office market is at a defining moment. Poised to cross the 1 billion sq ft threshold in 2025 with 0.99 billion sq ft already achieved India has become the world’s fourth-largest office market. This milestone speaks to the sheer scale of our commercial real estate, but more importantly, it underscores the sector’s resilience, institutional strength, and unwavering growth trajectory. Crossing this mark in 2025 highlights India’s ascent as one of the fastest-growing, most future-ready office markets globally a testament to our emergence as a true global office powerhouse.”

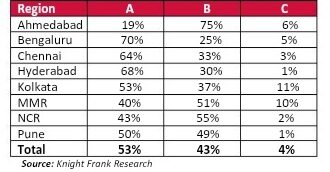

Grade-wise Composition of Office Buildings

India’s office market showcases a varied grade mix, with Grade A spaces being 53% of total supply, followed by Grade B at 43% and Grade C at 4%. Cities like Bengaluru, Hyderabad, and Chennai lead in Grade A stock due to strong IT and GCC demand. Legacy markets like Mumbai and NCR show a more equitable grade mix, reflecting slower transitions. Kolkata has the highest share of Grade C properties at 11%, highlighting asset upgrade needs. This distribution underscores the growing importance of asset repositioning and redevelopment in shaping the sector’s next growth phase.

India’s Office Sector Not Just Growing, But Evolving

India’s office market is evolving from sheer expansion to value-driven growth, marked by sustainable design, smart infrastructure, and tech integration. As the country strives to become a USD 10 tn economy by 2030, demand for modern, future-ready spaces will surge. Backed by a young digital workforce, low-dollar rents, and rising institutional interest, India is poised for inclusive, globally relevant growth.

With current office stock nearing 1 bn sq ft, India is poised to add its next billion square feet by 2036–2041, depending on the pace of expansion. These projections are not merely assumption-based; they are anchored in India’s expected nominal GDP growth, historical absorption trends, and increased institutionalisation of the office sector. At a 12.7% CAGR, supported by strong economic momentum and formalisation, the milestone could arrive by 2036.